At SBR we are going to be asked to apply our knowledge in practical situations. Here’s an example that involves a deep understanding of what it is that makes an investment an associate.

At SBR we are going to be asked to apply our knowledge in practical situations. Here’s an example that involves a deep understanding of what it is that makes an investment an associate.

At SBR we can often be involved in explaining which accounting standard is to be applied. Here is an example.…

The two are often confused – so let us thrash this out..

“If the company is factoring trade receivables then my understanding is that I am legally selling my trade receivables for an amount of cash less than the nominal. Say my debtors are $100,000 I might only get $90,000 from the factor – the bank. So I debit cash $90,000 – but what next?”

I take a look at the two methods of measuring NCI and the implications of goodwill.

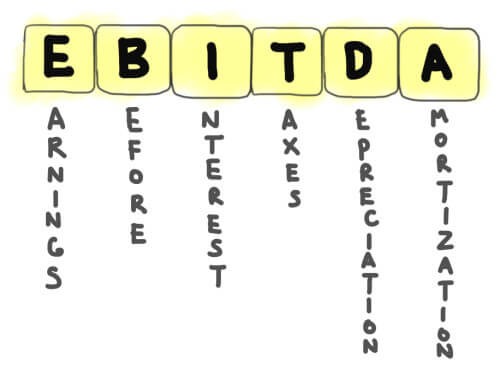

EBITDA is an Alternative Performance Measure. Here is an easy read that discusses its role in performance evaluation and interpretation

The vast majority of students who have sat RI exams successfully completed them without any technical issues. But some did experience technical issues. So, what can go wrong and what action can YOU take to minimise the risk of technical trouble on exam day.

Every course that my SBR online students do – whether that is tuition, revision or final mock – you do a mock exam. Here’s some examples of feedback.

This article assumes that you are basically familiar with IFRS2 Share based payments and is looking at a twist, which is how to account for options issued in a business combination.

When it comes to accounting for equity settled share based payments, there are a number of confusing issues. One is how the numbers are calculated when staff leave. A second confusion can arise when the issue relates to a business combination. This latter point will be addressed in a subsequent article.